Model Comparison Gallery¶

This gallery page showcases plots from k-diagram designed for comparing the performance of multiple models across various metrics, primarily using radar charts.

Note

You need to run the code snippets locally to generate the plot

images referenced below (e.g., images/gallery_model_comparison.png).

Ensure the image paths in the .. image:: directives match where

you save the plots (likely an images subdirectory relative to

this file).

Multi-Metric Model Comparison¶

The plot_model_comparison() function is

a tool for moving beyond single-score evaluations. It creates

a polar radar chart to visualize and compare multiple models across

several performance metrics simultaneously, providing a holistic

“fingerprint” of each model’s strengths and weaknesses.

First, let’s break down the components of this comparative plot.

Plot Anatomy

Angle (θ): Each angular axis represents a different performance metric (e.g., R², MAE, Training Time).

Radius (r): Corresponds to the normalized performance score for that metric, typically scaled to the range [0, 1]. To maintain consistency, all metrics are scaled such that a larger radius is always better (e.g., lower MAE or faster training time results in a larger radius).

Polygon: Each colored polygon represents a model, with its vertices showing its performance on each metric. The overall shape and size of the polygon provide an at-a-glance summary of the model’s performance profile.

With this framework, we can now apply the plot to a real-world model selection problem, progressing from a standard regression task to a more nuanced classification task.

Use Case 1: Standard Regression Model Comparison

The most common use for this plot is to select the best model for a standard regression task by balancing accuracy, error, and efficiency.

Let’s imagine an analytics team at an e-commerce company has built three different models to predict sales revenue: a fast but simple Ridge regression, a Lasso model that performs feature selection, and a more complex Decision Tree. They need to choose the best all-around performer.

1import kdiagram as kd

2import numpy as np

3import matplotlib.pyplot as plt

4

5# --- 1. Data Generation: Sales Revenue Forecast ---

6np.random.seed(42)

7n_samples = 100

8y_true_reg = np.random.rand(n_samples) * 50 + 10 # True revenue

9# Model 1 (Ridge): Good fit, fast

10y_pred_r1 = y_true_reg + np.random.normal(0, 4, n_samples)

11# Model 2 (Lasso): Similar fit, slightly slower

12y_pred_r2 = y_true_reg * 0.98 + 1 + np.random.normal(0, 4.5, n_samples)

13# Model 3 (Tree): Overfit, slower, poor on some metrics

14y_pred_r3 = y_true_reg + np.random.normal(2, 8, n_samples)

15

16times = [0.1, 0.3, 0.8] # Training times in seconds

17names = ['Ridge', 'Lasso', 'Tree']

18

19# --- 2. Plotting ---

20# Using default regression metrics: ['r2', 'mae', 'mape', 'rmse']

21kd.plot_model_comparison(

22 y_true_reg,

23 y_pred_r1, y_pred_r2, y_pred_r3,

24 train_times=times,

25 names=names,

26 title="Use Case 1: E-Commerce Sales Model Comparison",

27 scale='norm',

28 savefig="gallery/images/gallery_model_comparison_regression.png"

29)

30plt.close()

A radar chart showing the performance profiles of Ridge, Lasso, and Decision Tree models across five different metrics.¶

Use Case 2: Evaluating a Classification Task with a Custom Metric

This plot is equally usefull for classification. The default metrics will automatically switch to [‘accuracy’, ‘precision’, ‘recall’, ‘f1’], but we can also provide our own custom metrics to evaluate performance on criteria that are specific to our business problem.

Let’s consider a medical diagnosis model that predicts whether a patient has a rare disease. In this case, Recall (correctly identifying sick patients) is far more important than Precision. We can create a custom, weighted F-beta score to reflect this and add it to our plot.

1from sklearn.metrics import fbeta_score

2

3# --- 1. Data Generation: Medical Diagnosis ---

4np.random.seed(0)

5n_samples = 200

6y_true_clf = np.array([0] * 180 + [1] * 20) # Imbalanced data

7# Model A: High precision, but misses sick patients (low recall)

8y_pred_A = np.copy(y_true_clf)

9y_pred_A[np.random.choice(np.where(y_true_clf==1)[0], 12, False)] = 0

10# Model B: Lower precision, but finds most sick patients (high recall)

11y_pred_B = np.copy(y_true_clf)

12y_pred_B[np.random.choice(np.where(y_true_clf==0)[0], 20, False)] = 1

13

14# --- 2. Define a custom metric that prioritizes Recall ---

15# An F-beta score with beta=2 weighs recall higher than precision

16f2_score = lambda y_true, y_pred: fbeta_score(y_true, y_pred, beta=2)

17f2_score.__name__ = "F2-Score (Recall Focus)" # Give it a nice name for the plot

18

19# --- 3. Plotting with default and custom metrics ---

20kd.plot_model_comparison(

21 y_true_clf,

22 y_pred_A,

23 y_pred_B,

24 names=['Model A (High Precision)', 'Model B (High Recall)'],

25 metrics=['accuracy', 'precision', 'recall', f2_score], # Add our custom metric

26 title="Use Case 2: Medical Diagnosis Classifier Comparison",

27 scale='norm',

28 savefig="gallery/images/gallery_model_comparison_classification.png"

29)

30plt.close()

A radar chart showing how two classifiers perform on standard metrics as well as a custom “F2-Score” that prioritizes recall.¶

Best Practice

Don’t rely solely on default metrics. For real-world problems,

business needs often dictate that some errors are more costly than

others. Adding custom metrics to the plot_model_comparison

function, as shown in this use case, is a powerful way to ensure your

model evaluation aligns with your specific goals.

For a deeper understanding of the statistical concepts behind these evaluation metrics, please refer back to the main Multi-Metric Model Comparison (plot_model_comparison()) section.

Model Reliability (Calibration) Diagram¶

The plot_reliability_diagram() is the

industry-standard tool for assessing the calibration of a binary

classifier. It answers a crucial question: “When my model predicts a

70% probability of an event, does that event actually happen 70% of the

time?” A model whose probabilities accurately reflect real-world

frequencies is considered “well-calibrated” and is essential for making

trustworthy, risk-based decisions.

Let’s begin by breaking down the components of this fundamental plot.

Plot Anatomy

X-Axis (Mean Predicted Probability): For each bin, this is the average of the probabilities predicted by the model. This is also referred to as the forecast’s confidence.

Y-Axis (Observed Frequency): For each bin, this is the actual fraction of positive cases observed in the data. This is also referred to as the forecast’s accuracy.

Diagonal Line (\(y=x\)): This is the line of perfect calibration. A model whose points fall on this line is perfectly calibrated.

Counts Panel (Bottom): A histogram showing the number of predictions that fall into each probability bin, which helps in diagnosing if the model is timid (most predictions near 0.5) or decisive (most predictions near 0 or 1).

With this in mind, let’s explore how to use this plot to diagnose and compare the reliability of different models.

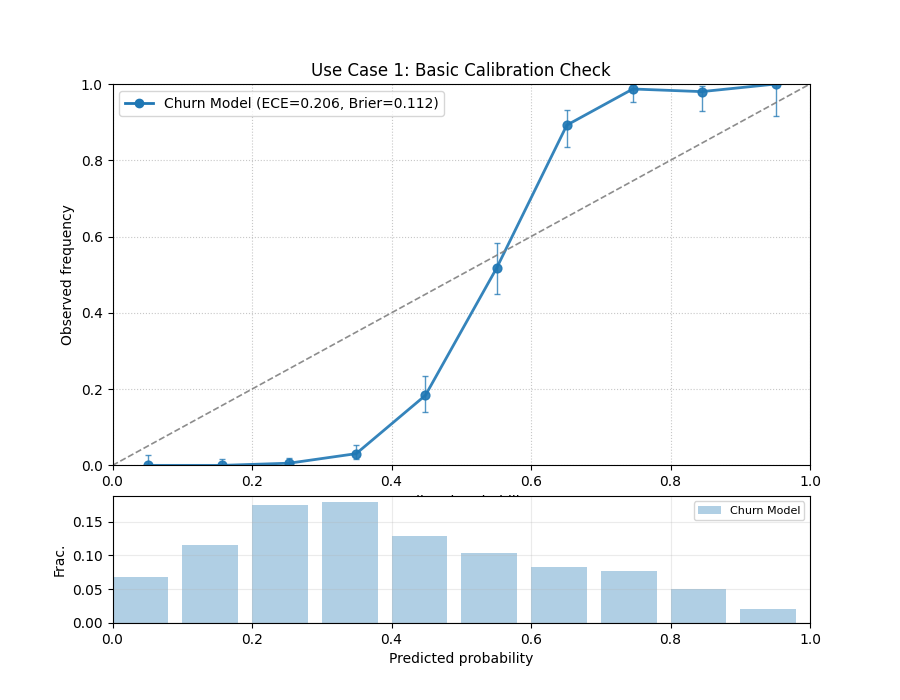

Use Case 1: Basic Calibration Check with Uniform Bins

The most common use case is to get a quick, initial assessment of a single model’s calibration. For this, we can use the default uniform binning strategy, which creates equally spaced bins across the [0, 1] probability range.

Let’s evaluate a model trained to predict customer churn, where a “1” means the customer is likely to leave.

1import kdiagram as kd

2import numpy as np

3import matplotlib.pyplot as plt

4

5# --- 1. Data Generation: Customer Churn Predictions ---

6np.random.seed(0)

7n_customers = 2000

8# True outcome: ~30% of customers churn

9y_true = (np.random.rand(n_customers) < 0.3).astype(int)

10# A reasonably good, but not perfect, model

11y_pred = np.clip(y_true * 0.4 + 0.3 + np.random.normal(0, 0.15, n_customers), 0.01, 0.99)

12

13# --- 2. Plotting ---

14kd.plot_reliability_diagram(

15 y_true, y_pred,

16 names=['Churn Model'],

17 n_bins=10,

18 strategy="uniform", # Default, but explicit here

19 title='Use Case 1: Basic Calibration Check',

20 savefig="gallery/images/gallery_reliability_diagram_basic.png"

21)

22plt.close()

A reliability diagram showing the model’s calibration curve relative to the perfect diagonal. The counts panel below shows the distribution of its predictions.¶

Use Case 2: Comparing Models with Quantile Binning

A more advanced task is to compare the reliability of multiple competing models. For this, quantile binning is often superior to uniform binning, as it ensures that each bin contains an equal number of samples, providing a more stable estimate of the observed frequency.

Let’s compare our “Churn Model” to a new “Calibrated Model” that has been post-processed to improve its reliability.

1# --- 1. Data Generation (uses y_true and y_pred from previous step) ---

2# Create a second, better-calibrated model's predictions

3y_pred_calibrated = np.clip(y_true * 0.35 + 0.32 + np.random.normal(0, 0.1, n_customers), 0.01, 0.99)

4

5# --- 2. Plotting ---

6kd.plot_reliability_diagram(

7 y_true, y_pred, y_pred_calibrated,

8 names=['Original Model', 'Calibrated Model'],

9 n_bins=12,

10 strategy="quantile", # Use quantile binning for a stable comparison

11 error_bars="wilson", # Add Wilson confidence intervals

12 title='Use Case 2: Comparing Model Reliability',

13 savefig="gallery/images/gallery_reliability_diagram_compare.png"

14)

15plt.close()

Two calibration curves are shown. The “Calibrated Model” (orange) hugs the diagonal line more closely than the “Original Model” (blue).¶

Best Practice

When comparing multiple models, using strategy="quantile" is

highly recommended. It prevents bins from being empty and provides

more stable and reliable estimates of the observed frequencies, leading

to a fairer comparison between models. Also, including error bars

(e.g., error_bars="wilson") provides crucial context about the

statistical uncertainty of your assessment.

See Also

For an alternative, and often more intuitive, way to visualize model

calibration, see the plot_polar_reliability()

function. It transforms this Cartesian plot into a polar spiral,

which can make miscalibration patterns even easier to spot.

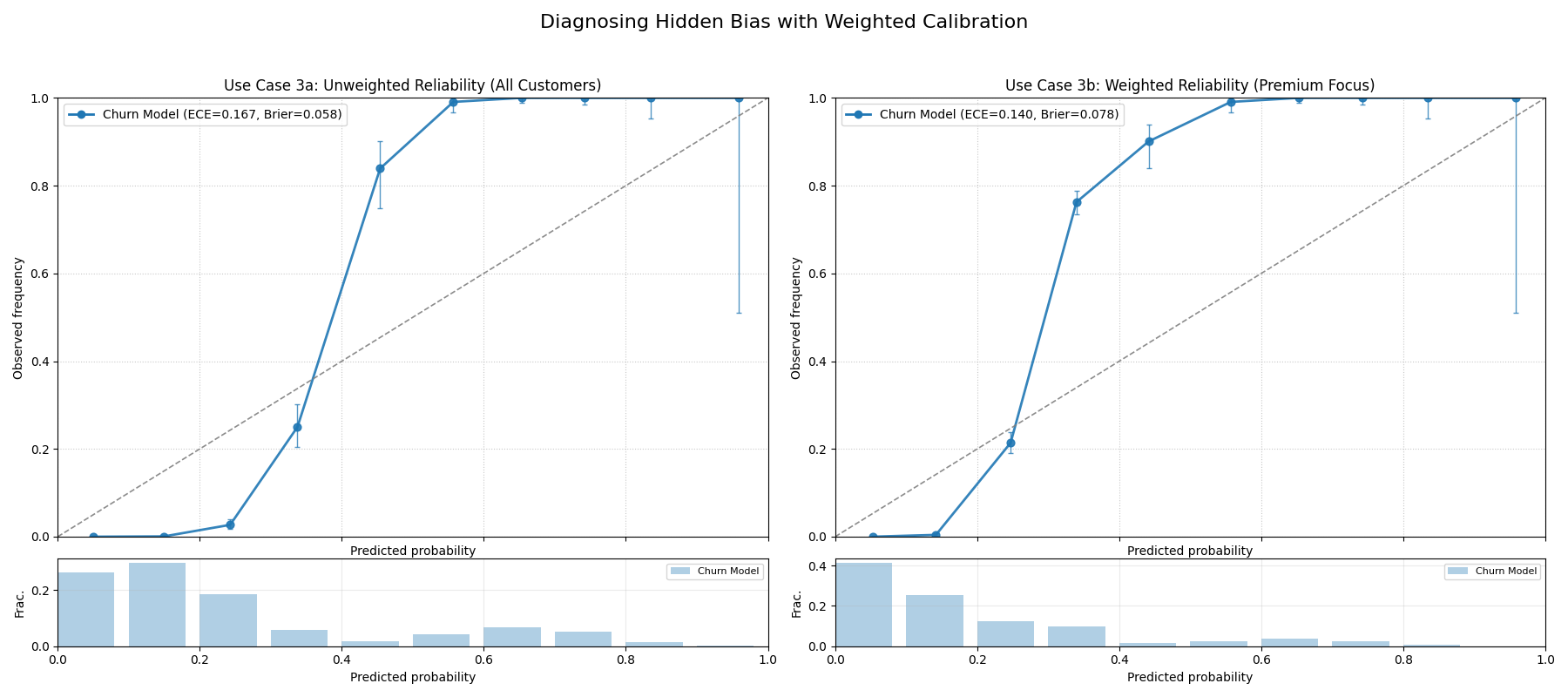

Use Case 3: Weighted Calibration for High-Value Segments

In many real-world business problems, not all prediction errors are

created equal. An error on a high-value customer can be far more costly

than an error on a standard customer. A model might appear well-calibrated

overall, but this aggregate view can hide poor performance on the most

critical segments. The sample_weight parameter is a powerful tool

for diagnosing this exact problem.

Best Practice

When the business impact of your model’s predictions is not uniform

across all samples, always perform a weighted calibration analysis.

Use the sample_weight parameter to assign higher importance to

high-value customers, critical events, or costly failure modes to

ensure your model is reliable where it matters most.

Let’s tackle a common problem in customer retention: ensuring our churn model is reliable for our most valuable “premium” subscribers.

Practical Example

A streaming service uses a model to predict the probability that a subscriber will churn (cancel their subscription). The model’s overall calibration appears to be good. However, the business is most concerned about retaining its “premium” subscribers, as they account for a disproportionate amount of revenue. Is the model’s churn probability trustworthy specifically for this high-value segment?

We will create a side-by-side comparison. The left plot will show

the standard, unweighted reliability, while the right plot will use

sample_weight to give 10x more importance to the premium

subscribers, revealing the model’s true performance for this

critical group.

1import kdiagram as kd

2import numpy as np

3import pandas as pd

4import matplotlib.pyplot as plt

5

6# --- 1. Data Generation: Churn with a high-value segment ---

7np.random.seed(10)

8n_customers = 5000

9# True churn status

10y_true = (np.random.rand(n_customers) < 0.2).astype(int)

11# Create sample weights: 10% are "premium" customers with 10x weight

12sample_weight = np.ones(n_customers)

13premium_indices = np.random.choice(n_customers, 500, replace=False)

14sample_weight[premium_indices] = 10

15

16# --- 2. Create biased predictions FOR THE PREMIUM SEGMENT ---

17# The model is well-calibrated for standard users but overconfident

18# for premium users (predicts lower churn probability than is real)

19y_pred = np.clip(y_true * 0.5 + 0.15 + np.random.normal(0, 0.1, n_customers), 0.01, 0.99)

20# Introduce the bias for the premium segment

21y_pred[premium_indices] *= 0.5

22

23# --- 3. Create side-by-side plots ---

24fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(18, 8))

25

26kd.plot_reliability_diagram(

27 y_true, y_pred,

28 ax=ax1,

29 names=['Churn Model'],

30 title='Use Case 3a: Unweighted Reliability (All Customers)',

31 savefig=None # Prevent saving from the first call

32)

33kd.plot_reliability_diagram(

34 y_true, y_pred,

35 ax=ax2,

36 sample_weight=sample_weight, # Apply the crucial sample weights

37 names=['Churn Model'],

38 title='Use Case 3b: Weighted Reliability (Premium Focus)',

39 savefig=None # Prevent saving from the second call

40)

41

42fig.suptitle('Diagnosing Hidden Bias with Weighted Calibration', fontsize=16)

43fig.tight_layout(rect=[0, 0, 1, 0.95])

44fig.savefig("gallery/images/gallery_reliability_diagram_weighted.png")

45plt.close(fig)

A two-panel figure. The left plot (unweighted) shows a reasonably well-calibrated model. The right plot (weighted by customer value) reveals the same model is severely overconfident for its most important customers.¶

For a deeper understanding of the statistical theory behind calibration and proper scoring rules, please refer back to the main Reliability Diagram (plot_reliability_diagram()) section.

Polar Reliability Diagram (Calibration Spiral)¶

The plot_polar_reliability() function

provides a novel and highly intuitive visualization of model calibration.

It transforms the traditional reliability diagram into a “calibration

spiral,” where deviations from a perfect spiral immediately reveal the

nature and location of a model’s miscalibrations through diagnostic

coloring.

First, let’s break down the components of this innovative plot.

Plot Anatomy

Angle (θ): Represents the mean predicted probability (\(\bar{p}_k\)) for each bin, sweeping from 0.0 at 0° to 1.0 at 90°. This is the model’s confidence.

Radius (r): Represents the observed frequency of the event (\(\bar{y}_k\)) for each bin. This is the actual outcome.

Perfect Calibration Spiral: The dashed black line represents the ideal case where \(r = \frac{2\theta}{\pi}\) (\(\bar{y}_k = \bar{p}_k\)). A model’s spiral should lie directly on this line.

Color: The color of the model’s spiral is a diagnostic tool, representing the calibration error (\(\bar{y}_k - \bar{p}_k\)). Colors on one side of the colormap’s center (e.g., reds) indicate over-confidence, while colors on the other side (e.g., blues) indicate under-confidence.

With this in mind, let’s apply the plot to a real-world problem to see how it uncovers different types of miscalibration.

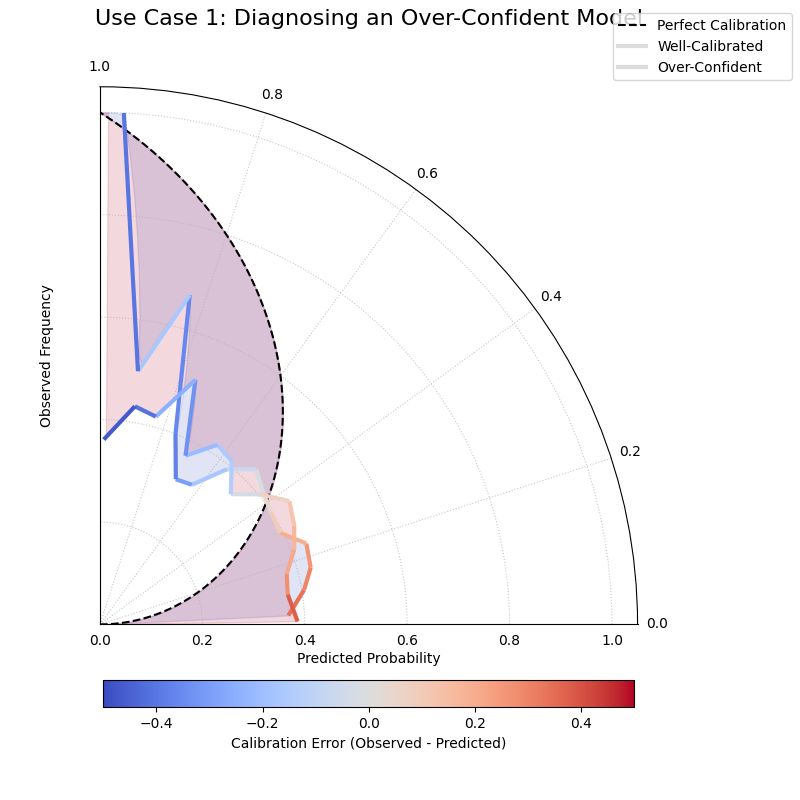

Use Case 1: Diagnosing an Over-Confident Model

A common failure mode for classifiers, especially on complex tasks, is overconfidence. The model assigns high probabilities to its predictions, but its real-world accuracy doesn’t match this high level of certainty.

Let’s simulate a scenario in medical diagnostics, where a model is trained to predict the probability of a disease. An overconfident model might predict a 90% probability of disease when the actual rate for such patients is only 70%, which could lead to unnecessary treatments.

1import kdiagram as kd

2import numpy as np

3import matplotlib.pyplot as plt

4

5# --- 1. Data Generation: A Well-Calibrated vs. Over-Confident Model ---

6np.random.seed(0)

7n_samples = 2000

8# The true probability of the event is 0.4

9y_true = (np.random.rand(n_samples) < 0.4).astype(int)

10

11# A well-calibrated model's probabilities are realistic

12calibrated_preds = np.clip(0.4 + np.random.normal(0, 0.15, n_samples), 0, 1)

13

14# An over-confident model pushes probabilities towards the extremes of 0 and 1

15overconfident_preds = np.clip(0.4 + np.random.normal(0, 0.3, n_samples), 0, 1)

16

17# --- 2. Plotting ---

18kd.plot_polar_reliability(

19 y_true,

20 calibrated_preds,

21 overconfident_preds,

22 names=["Well-Calibrated", "Over-Confident"],

23 n_bins=15,

24 cmap='coolwarm',

25 title="Use Case 1: Diagnosing an Over-Confident Model",

26 savefig="gallery/images/gallery_polar_reliability_overconfident.png"

27)

28plt.close()

The “Well-Calibrated” model’s spiral closely follows the dashed reference line, while the “Over-Confident” model’s spiral falls inside the reference.¶

See Also

This plot is the polar-coordinate counterpart to the traditional

Cartesian plot_reliability_diagram().

While both show the same underlying data, the spiral format can often

make deviations and the nature of miscalibration more intuitive to

see at a glance.

For a deeper understanding of the statistical theory behind calibration and reliability, please refer back to the main Polar Reliability Diagram (plot_polar_reliability()) section.

Comparing Metrics Across Horizons¶

The plot_horizon_metrics() function

creates a polar bar chart designed to compare two key metrics across a

set of distinct categories, such as different forecast horizons. It’s a

powerful tool for visualizing how a model’s uncertainty (bar height)

and central tendency (bar color) evolve over time or differ between

groups.

First, let’s break down the components of this two-dimensional summary plot.

Plot Anatomy

Angle (θ): Each angular sector represents a distinct category or horizon (e.g., “H+1”, “H+2”), corresponding to a row in the input DataFrame. The labels for these sectors are provided via the

xtick_labelsparameter.Radius (r): The height of each bar represents the average value of a primary metric. By default, this is the mean prediction interval width (\(Q_{upper} - Q_{lower}\)).

Color: The color of each bar visualizes a secondary metric. By default, this is the mean of the median (Q50) predictions for that category, adding another layer of information to the comparison.

With this in mind, let’s apply the plot to a classic forecasting problem.

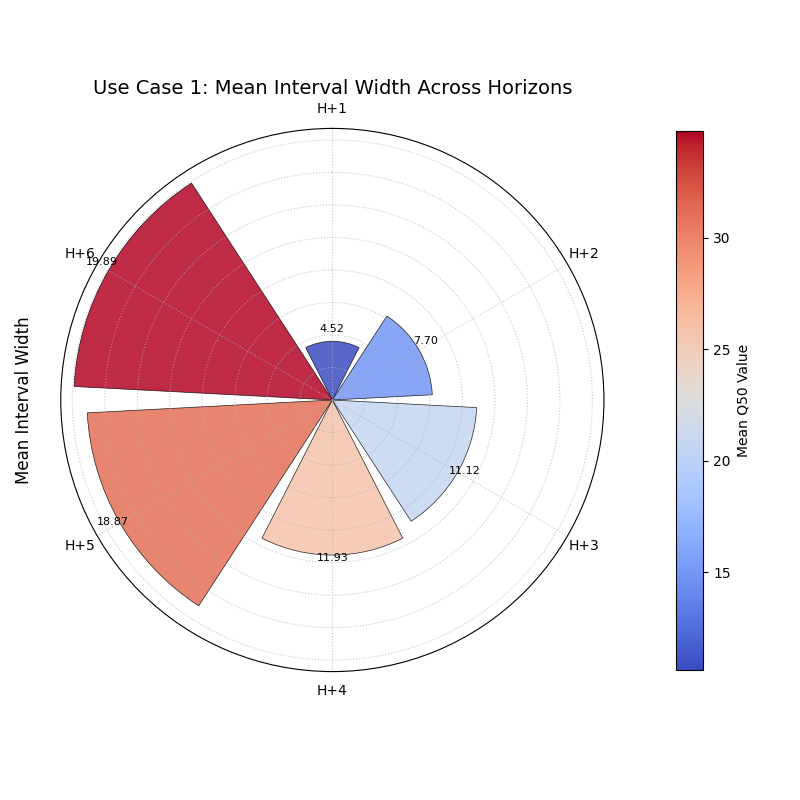

Use Case 1: Standard Forecast Horizon Analysis

The most common use of this plot is to see how a model’s uncertainty and central prediction change as it forecasts further into the future. It’s a typical and expected behavior for uncertainty to grow over longer lead times, and this plot quantifies that drift.

Let’s simulate a multi-step forecast where both the predicted value and its uncertainty increase for each step.

1import kdiagram as kd

2import pandas as pd

3import numpy as np

4import matplotlib.pyplot as plt

5

6# --- 1. Data Generation: Multi-step Forecast ---

7# Each row represents a forecast horizon (H+1 to H+6)

8# Each column is a different sample of that forecast

9horizons = ["H+1", "H+2", "H+3", "H+4", "H+5", "H+6"]

10df = pd.DataFrame(index=horizons)

11q10_cols, q90_cols, q50_cols = [], [], []

12

13for i in range(len(horizons)):

14 # Both median and width increase with the horizon

15 median = 10 + 5 * i

16 width = 5 + 3 * i

17 # Create two samples for each horizon

18 df[f'q10_s{i}_1'] = median - width/2 + np.random.randn()

19 df[f'q90_s{i}_1'] = median + width/2 + np.random.randn()

20 df[f'q50_s{i}_1'] = median + np.random.randn()

21 df[f'q10_s{i}_2'] = median - width/2 + np.random.randn()

22 df[f'q90_s{i}_2'] = median + width/2 + np.random.randn()

23 df[f'q50_s{i}_2'] = median + np.random.randn()

24 q10_cols.extend([f'q10_s{i}_1', f'q10_s{i}_2'])

25 q90_cols.extend([f'q90_s{i}_1', f'q90_s{i}_2'])

26 q50_cols.extend([f'q50_s{i}_1', f'q50_s{i}_2'])

27

28# Reshape for the function: rows are horizons, cols are samples

29df_horizons = pd.DataFrame(index=horizons)

30for i in range(len(horizons)):

31 df_horizons.loc[f"H+{i+1}", 'q10_s1'] = df.loc[f"H+{i+1}", f'q10_s{i}_1']

32 df_horizons.loc[f"H+{i+1}", 'q90_s1'] = df.loc[f"H+{i+1}", f'q90_s{i}_1']

33 df_horizons.loc[f"H+{i+1}", 'q50_s1'] = df.loc[f"H+{i+1}", f'q50_s{i}_1']

34 df_horizons.loc[f"H+{i+1}", 'q10_s2'] = df.loc[f"H+{i+1}", f'q10_s{i}_2']

35 df_horizons.loc[f"H+{i+1}", 'q90_s2'] = df.loc[f"H+{i+1}", f'q90_s{i}_2']

36 df_horizons.loc[f"H+{i+1}", 'q50_s2'] = df.loc[f"H+{i+1}", f'q50_s{i}_2']

37

38# --- 2. Plotting ---

39kd.plot_horizon_metrics(

40 df=df_horizons,

41 qlow_cols=['q10_s1', 'q10_s2'],

42 qup_cols=['q90_s1', 'q90_s2'],

43 q50_cols=['q50_s1', 'q50_s2'],

44 title="Use Case 1: Mean Interval Width Across Horizons",

45 xtick_labels=horizons,

46 r_label="Mean Interval Width",

47 cbar_label="Mean Q50 Value",

48 savefig="gallery/images/gallery_horizon_metrics_basic.png"

49)

50plt.close()

A polar bar chart where both the height of the bars (uncertainty) and their color (median prediction) increase progressively across the forecast horizons.¶

See Also

This plot is closely related to

plot_model_drift(). While both

visualize drift over horizons with polar bars, this function is more

general-purpose. It can be used to compare any set of distinct

categories (not just time horizons) and offers more direct control

over the data columns used for the radius and color calculations.

For a deeper understanding of the statistical concepts behind analyzing forecasts over different horizons, please refer back to the main Comparing Metrics Across Horizons (plot_horizon_metrics()) section.

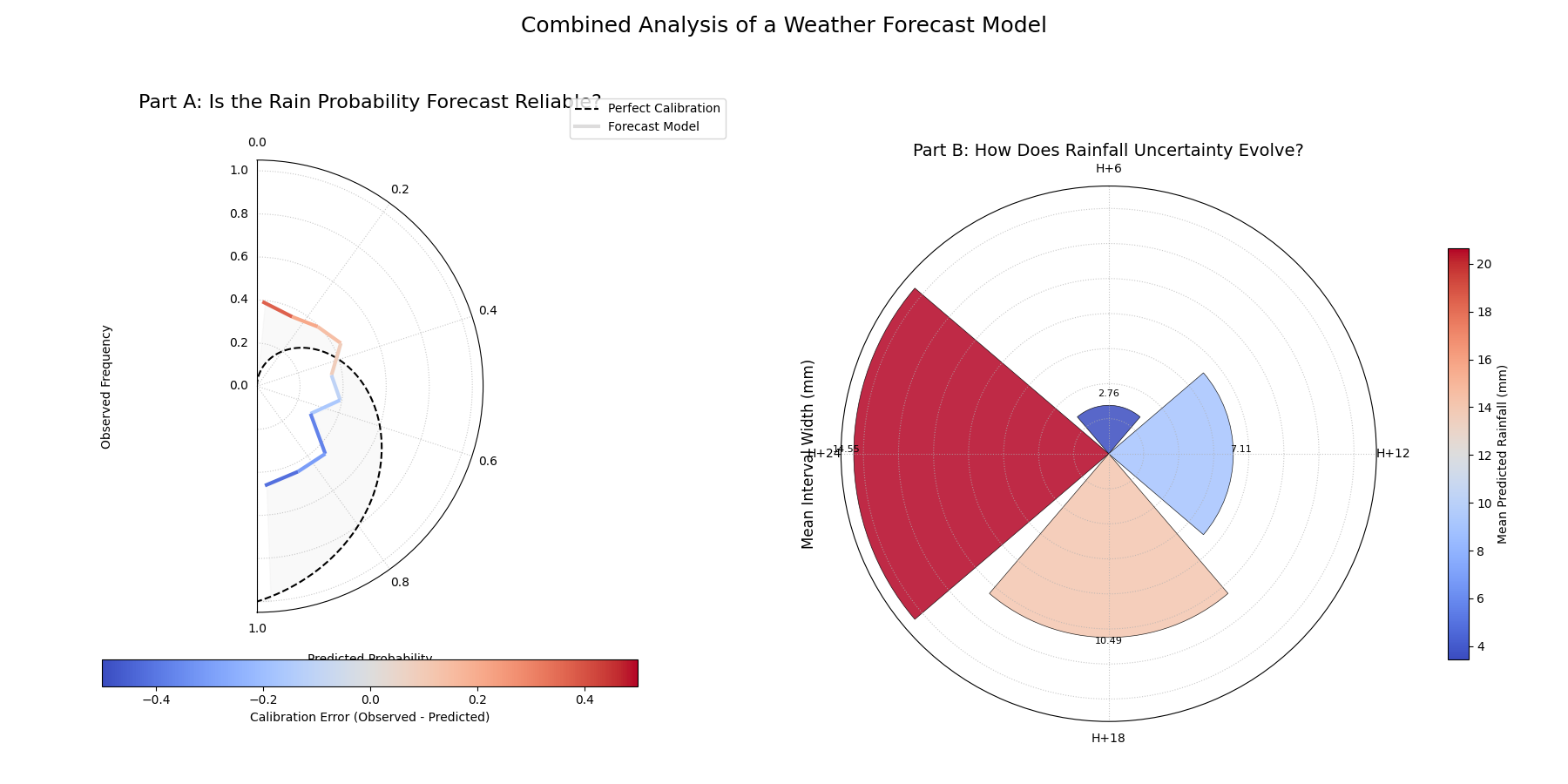

Combined Analysis: Reliability and Horizon Drift¶

Evaluating a sophisticated forecasting model often requires more than a

single plot. A comprehensive analysis involves using multiple,

complementary visualizations to diagnose different aspects of performance.

This tutorial showcases a workflow, combining

plot_polar_reliability() and

plot_horizon_metrics() to perform a

two-part evaluation of a weather forecast.

First, let’s re-introduce the anatomy of the two plots we will be using in our combined analysis.

Plot Anatomy (Polar Reliability)

Angle (θ): Represents the mean predicted probability of an event (e.g., rain), sweeping from 0.0 to 1.0.

Radius (r): Represents the observed frequency of that event.

Reference: The dashed black spiral is the line of perfect calibration. A good model’s curve should follow this spiral.

Plot Anatomy (Horizon Metrics)

Angle (θ): Represents distinct forecast horizons (e.g., “H+6”, “H+12”).

Radius (r): The height of each bar represents the average prediction interval width (uncertainty).

Color: The color of each bar represents the average median (Q50) prediction (e.g., the expected amount of rain).

Now, let’s apply these two diagnostics to a challenging, real-world forecasting problem.

Use Case: A Holistic Evaluation of a Weather Forecast Model

A meteorological agency has a new weather model that produces two key outputs for a 24-hour period:

The probability that it will rain at all (a binary event).

A probabilistic forecast of the total rainfall amount (in mm).

To validate this new model, we need to answer two critical questions:

Is the model reliable? When it predicts a 70% chance of rain, is it trustworthy?

How does its uncertainty grow over time? Is the forecast for rainfall amount sharp and useful for the next 6 hours, but too uncertain for the full 24-hour period?

We will perform a combined analysis by creating a side-by-side plot to answer both questions at once.

Practical Example

1import kdiagram as kd

2import pandas as pd

3import numpy as np

4import matplotlib.pyplot as plt

5

6# --- 1. Data Generation ---

7np.random.seed(1)

8n_days = 1000

9

10# --- Part A: Data for Reliability Plot (Probability of Rain) ---

11# True events: It rains on 40% of days

12y_true_rain_event = (np.random.rand(n_days) < 0.4).astype(int)

13# A slightly over-confident model for predicting the event

14y_pred_rain_prob = np.clip(0.4 + np.random.normal(0, 0.3, n_days), 0, 1)

15

16# --- Part B: Data for Horizon Metrics Plot (Amount of Rain) ---

17horizons = ["H+6", "H+12", "H+18", "H+24"]

18df_horizons = pd.DataFrame(index=horizons)

19# For each horizon, we have multiple samples (e.g., from different days)

20n_samples = 50

21q10_cols, q90_cols, q50_cols = [], [], []

22

23for i in range(len(horizons)):

24 # Both median rainfall and uncertainty increase with the horizon

25 median = 5 + 5 * i

26 width = 3 + 4 * i

27 # Create two samples for each horizon

28 df_horizons.loc[f"H+{6*(i+1)}", 'q10_s1'] = median - width/2 + np.random.randn()

29 df_horizons.loc[f"H+{6*(i+1)}", 'q90_s1'] = median + width/2 + np.random.randn()

30 df_horizons.loc[f"H+{6*(i+1)}", 'q50_s1'] = median + np.random.randn()

31 df_horizons.loc[f"H+{6*(i+1)}", 'q10_s2'] = median - width/2 + np.random.randn()

32 df_horizons.loc[f"H+{6*(i+1)}", 'q90_s2'] = median + width/2 + np.random.randn()

33 df_horizons.loc[f"H+{6*(i+1)}", 'q50_s2'] = median + np.random.randn()

34

35# --- 2. Create a figure with two polar subplots ---

36fig = plt.figure(figsize=(18, 9))

37ax1 = fig.add_subplot(1, 2, 1, projection='polar')

38ax2 = fig.add_subplot(1, 2, 2, projection='polar')

39

40# --- 3. Plot each diagnostic on its dedicated axis ---

41kd.plot_polar_reliability(

42 y_true_rain_event, y_pred_rain_prob,

43 ax=ax1,

44 names=["Forecast Model"],

45 title='Part A: Is the Rain Probability Forecast Reliable?'

46)

47kd.plot_horizon_metrics(

48 df=df_horizons,

49 ax=ax2,

50 qlow_cols=['q10_s1', 'q10_s2'],

51 qup_cols=['q90_s1', 'q90_s2'],

52 q50_cols=['q50_s1', 'q50_s2'],

53 xtick_labels=horizons,

54 title='Part B: How Does Rainfall Uncertainty Evolve?',

55 r_label="Mean Interval Width (mm)",

56 cbar_label="Mean Predicted Rainfall (mm)"

57)

58

59fig.suptitle('Combined Analysis of a Weather Forecast Model', fontsize=18)

60fig.tight_layout(rect=[0, 0.03, 1, 0.95])

61fig.savefig("gallery/images/gallery_comparison_combined.png")

62plt.close(fig)

A two-panel figure providing a complete model evaluation. The left plot diagnoses the calibration of the rain probability forecast, while the right plot shows how the uncertainty of the rainfall amount forecast grows over time.¶

For a deeper understanding of the statistical concepts behind these evaluation techniques, please refer back to the main Model Comparison Visualization and Evaluating Probabilistic Forecasts sections.